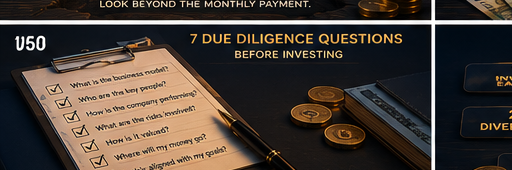

Every year, Filipinos lose billions of pesos to investment scams, poorly understood products, and promises that sounded reasonable until they weren’t. The people who got hurt were not all naive. Many were educated, employed, and careful with money in every other area of their lives. What they often lacked were the right questions to ask before signing or sending anything. These seven questions apply to everything: stocks, UITFs, REITs, digital banks, paluwagan, networking schemes, real estate pre-selling, cooperatives, and anything else being pitched to you by anyone.

1. Is this registered with the SEC or BSP?

In the Philippines, companies that offer investment products to the public are required to be registered with the Securities and Exchange Commission (SEC). Banks and financial institutions are regulated by the Bangko Sentral ng Pilipinas (BSP). Before putting money anywhere, verify registration directly — not through a link the seller gives you, but by going to sec.gov.ph or bsp.gov.ph yourself and searching for the company name. Registration is not a guarantee that an investment is good, but the absence of registration is an immediate stop sign. If someone cannot point you to a verifiable SEC or BSP registration, you are done with that conversation.

2. Who gets paid when I invest — and how much?

Every investment product has a cost structure. Find out: is there a selling commission, a management fee, an annual fee, a performance fee? Who receives it? A broker, an agent, the fund manager? Commission-based sellers have an incentive to recommend what earns them the most — not what is best for you. This is not automatically bad, but it needs to be transparent. If the person presenting the investment cannot clearly explain how they are compensated, that is a problem. Understanding the fee structure also helps you calculate your real return after costs are deducted.

3. What is the realistic return range — not the best case?

Any investment can show you its best historical performance. Ask instead: what is the range? What happened in a bad year? What is the average over five or ten years, not just the most recent period when prices were rising? For regulated products like UITFs, the fund’s NAVPU history is publicly available and updated daily. For newer products or anything being pitched informally, the absence of a range — the insistence on a single promised return — is a major warning sign. Returns above 12-15% annually with low stated risk should be questioned carefully. That range is not impossible, but it requires taking on significant risk that the seller should be disclosing.

4. Can I get my money back — and exactly when?

Liquidity matters as much as return. Some investments have lock-in periods: MP2 has a five-year term, time deposits have specific maturity dates with penalties for early withdrawal, some UITFs have holding periods. Others are liquid: stocks can be sold any trading day, some digital bank savings have no lock-in. Understanding when you can access your money — and under what conditions — is not a detail to read later. It is a core question. For informal investments like paluwagan or cooperative shares, ask in writing: what is the exact process for withdrawal, and how long does it take?

5. What is the worst-case scenario for this investment?

A legitimate investment opportunity can answer this question. The worst case for a time deposit is that the bank fails — and deposits up to P500,000 are insured by PDIC (Philippine Deposit Insurance Corporation, pdic.gov.ph). The worst case for a UITF or stock is that you lose a significant portion of your principal during a market downturn. The worst case for an unregistered investment scheme is that you lose everything and have no legal recourse. Ask the question plainly. If the person pitching to you cannot name a realistic downside, either they don’t understand what they’re selling, or they are not being honest with you.

6. Who else has invested — and can you verify their experience independently?

Social proof is one of the most effective tools scammers use. Testimonials, success stories, Facebook screenshots, friends-of-friends who “already made money” — these are easy to manufacture and impossible to verify when they come from the same source trying to get your money. Ask instead: can you give me the name and contact information of someone who has been invested for more than a year, who I can contact independently? If every reference runs through the same person or group, it is not independent verification. Reach out separately. Ask what their actual experience has been with withdrawals, not just deposits.

7. What happens to my money if this company closes?

Regulated investments have answers to this question. UITF assets are held in trust, separate from the bank’s own funds — if the bank closes, UITF holders are protected. Stocks held through a broker are registered in your name with the PSE depository (PDTC). Insurance policies are backed by the Insurance Commission’s liquidation framework. But for unregulated or informal investment products, the answer is often: nothing. Your money is gone. Ask the question before you invest — not after.

Scams don’t look like scams. They look like opportunities with urgency and a smiling person behind them.