You have been counting the years. Maybe the months. You tell yourself one more contract, then I am going home for good. But the question that quietly sits underneath all of that is one most OFWs avoid asking directly: are you actually ready, financially, to leave?

Not ready emotionally. Not ready because you are tired. Financially ready. Because going home without a real financial foundation does not mean the sacrifice stops. It often means the pressure just moves to a different person, or comes back to you in a different form.

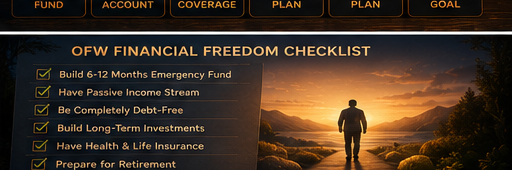

Here are five signs that you have genuinely crossed that line. This is a high bar. Most OFWs who return home do not meet all five at the same time. That is not a judgment. It is just the honest picture.

1. You are debt-free, or close enough to have a clear finish line

This does not mean you need to have zero debt the day you board your last flight home. It means your remaining debt has a concrete repayment timeline, your monthly obligations are manageable on a local income, and you are not carrying any high-interest consumer debt that will compound on you once your OFW salary is gone.

If you still have significant credit card balances, personal loans, or informal debt that you have been managing only because of your current income abroad, returning home before resolving those puts you at serious risk of going back into the cycle. The goal is not perfection. The goal is a finish line you can actually see.

2. You have income at home that does not depend on your remittance

This is the sign most OFWs skip. They think: I have savings, so I am fine. Savings are not income. Savings run out.

Before you leave for good, you need some form of earning power in the Philippines: a small business generating consistent revenue, a rental property with actual paying tenants, freelance or consulting work, or a job offer you have already accepted. The income does not need to match your OFW salary immediately. But it needs to exist and to cover at least your basic monthly expenses at home.

If your only plan is to “figure it out when I get there,” that is not a plan. That is hope.

3. Your family is not solely dependent on your remittance

One of the most overlooked financial risks an OFW carries is being the only income source for an entire household. If your family at home has structured their entire lifestyle around your monthly transfer, stopping that transfer — even with savings to cushion it — creates immediate pressure.

This sign is really about preparation: have you had honest conversations with your family about adjusting their budget? Have dependents been given a transition plan? Is there at least one other income earner in the household? This is not about being selfish with your money. It is about making sure your return does not trigger a financial emergency for the people you came home for.

4. You have an emergency fund that stays intact

An emergency fund is 3 to 6 months of your total household expenses held in a liquid account, meaning you can access it within a few business days without penalty. This fund is separate from your savings, separate from your investment accounts, and separate from the money you are using to settle debt.

Many OFWs have savings but no true emergency fund, because all of it is earmarked for something: a house, a debt, a child’s tuition. When you go home, unexpected things will happen. A family member will get sick. A business will take longer than expected to earn. Your emergency fund is what keeps you from going back into debt when life does not follow the plan.

5. You have health coverage arranged for yourself and your dependents

This one gets overlooked completely until someone gets sick. When you are an active OFW, you may have health coverage through your employer or through your OWWA membership. The moment your contract ends, that coverage ends with it.

Before your last contract is up, you need a clear answer to this question: who pays for hospitalization if someone in my family needs it next month? Options include an active PhilHealth membership with updated contributions (contributions and benefit structures change, so verify current rates and coverage at philhealth.gov.ph), a private HMO plan, or company health coverage if you are transitioning to local employment. None of these are expensive to arrange while you still have an OFW income. All of them become expensive to arrange after something goes wrong.

Meeting all five of these before you board that last flight is the goal. If you are not there yet, that is useful information, not a reason to give up — it tells you exactly what needs to happen before you can go home without looking over your shoulder.

Going home should feel like an arrival, not an escape.