You saved up. Maybe it took six months, maybe a year. It feels significant — and it is. Now comes the question almost nobody asks out loud: what do you actually do with it?

Most financial content will tell you to invest immediately. Open a stock account, buy REITs, put it in UITF. And those are not bad tools. But if that’s the first thing you do with your first real savings, you are skipping steps that matter more. This post is about the order, because the order is what protects the money you worked for.

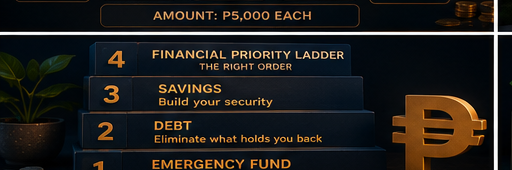

1. Pay off high-interest debt first

If you are carrying a credit card balance, a 5-6 loan, or an active digital lending app balance, your first savings should go there before anywhere else. The math is simple: a credit card in the Philippines charges 2% to 3% per month in interest (that is 24% to 36% per year as of 2026 — verify current rates with your bank or BSP advisory). No legitimate investment guarantees returns that match that rate. Paying down that debt is effectively earning 24% to 36% risk-free. It does not feel like progress because you are not building a balance anywhere — but your net worth is improving with every peso you apply to high-interest debt.

This applies to informal loans too. If you borrowed from someone charging above-market interest, that is your highest-priority use of new savings.

2. Fully fund your emergency fund

Before you invest a single peso, you need three to six months of living expenses sitting in a liquid, accessible account — not invested, not locked. A regular savings account or a high-yield savings account works. The emergency fund is not a savings goal. It is insurance against a crisis forcing you back into debt. If you skip this step and your phone breaks, someone in your family needs hospitalization, or you lose your job — you will borrow again. And borrowing to replace money you put into investments defeats the purpose of investing.

Most OFWs in debt have never had this buffer. Building it first is the unsexy work that prevents the cycle from restarting.

3. Start or continue your MP2 contribution

Once high-interest debt is cleared and your emergency fund is complete, Pag-IBIG MP2 is one of the most reliable and accessible options for OFWs. As of recent years, MP2 has paid annual dividends in the 6% to 7% range — higher than most savings accounts and time deposits. Your contributions are locked for five years, but the money is not at risk in the way equities are. OFWs can open and contribute to MP2 online through the Pag-IBIG Fund portal. (Check the official Pag-IBIG website for current dividend declarations and contribution guidelines, as these change annually.)

This step belongs here — after debt and emergency fund — because the five-year lock-in is manageable once you have a cash buffer. Before that buffer exists, locking money away creates vulnerability.

4. Time deposit or Treasury bills for medium-term goals

If you have a goal within two to four years — a small business fund, property down payment, a trip home that costs real money — a time deposit or a Treasury bill (T-bill) through the Bureau of the Treasury’s online platform is a better fit than equities. T-bills are government-backed, short-term (91, 182, or 364 days), and carry no market risk. Time deposits at Philippine banks typically range from 30 days to five years.

Returns are modest — often in the 4% to 6% range depending on the instrument and market conditions as of 2026 — but the goal of this step is not maximum return. The goal is parking money that has a purpose in a place where it cannot be eroded by impulse spending or volatility.

5. Only now consider other investments

After all four steps above, you are genuinely ready to look at UITFs, REITs, dividend stocks, or other investment vehicles. Not because the earlier steps are more important forever, but because they are foundational. Investing in equities when you have unpaid high-interest debt is like filling a bucket with a hole in it. Investing without an emergency fund is like building on a floor that might not hold.

At this stage, research the options carefully. Understand fees, minimum holding periods, and risks before putting money in. There is no urgency. The urgency was in steps one and two.

The order is what protects you — not how much you save, but where it goes first.

(Note: Interest rates, dividend declarations, and product terms change. Always verify current figures directly with BSP, Pag-IBIG, or your bank before making decisions.)